Orygen Perú S.A.A. published its unaudited separate financial statements for the first quarter of 2026.

“The first-quarter results reflect a challenging period for the company. We saw the expiration of several long-standing commercial contracts and were impacted by the natural gas supply crisis, which drove up production costs. Despite this, we are maintaining the pace of our investment plan with Wayra Solar, which is more than 70% complete as of Q1 and is expected to begin commercial operations by the end of this year. This project will be Peru’s first large-scale hybrid complex and will allow us to continue delivering sustainable, reliable, and competitive energy to our customers,” said Marco Fragale, CEO of Orygen.

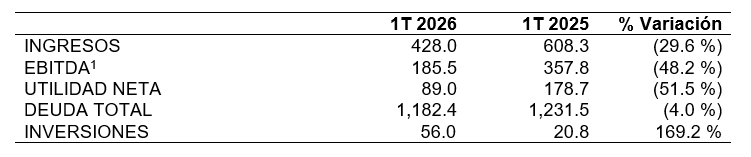

MAIN FINANCIAL INDICATORS (Expressed in millions of Soles)

- REVENUE Revenues decreased by S/. 180.3 million (-29.6% Q3-YTD) compared to the same period last year, primarily due to the expiration of older contracts with regulated and non-regulated customers, which had higher volumes and prices than the newly contracted agreements.

- EBITDA Revenue decreased by S/. 172.3 million (-48.2% YoY) compared to the same period last year, due to lower gross profit[1] in S/. 183.7 million, mainly explained by the aforementioned drop in income and slightly higher generation costs —despite lower sales volume—, associated with the incident in the gas pipeline reported by TGP in March, which implied increased diesel usage for 13 days to sustain thermal generation. This effect was partially offset by: (i) a reduction in administrative expenses[2] of S/ 6.6 million, after the completion of the technological transition project in 2025, among other administrative efficiencies and (ii) higher other income of S/ 4.9 million from the sale of company assets.

- NET INCOMEIt decreased by S/. 92.0 million compared to the same period of the previous year, mainly due to lower operating profit of S/. 172.5 million linked to the previously discussed factors, partially offset by: (i) higher net financial income of S/. 42.1 million associated with the declaration of dividends by the subsidiary Chinango in March (compared to the previous year, when such declaration took place in April), and lower interest following the resolution in 2025 of administrative processes with SUNAT; (ii) higher foreign exchange gains of S/. 10.6 million explained by an active monetary position in dollars in a context of dollar appreciation against the sol between December 2025 and March 2026; and (iii) lower income tax expenses of S/. 27.8 million, supported by lower profit before taxes.

- TOTAL DEBT: It decreased by S/ 49.1 million, primarily due to the depreciation of the U.S. dollar between March 2025 and March 2026, given that the debt is primarily denominated in that currency. This effect was partially offset by: (i) higher interest accrued on the intercompany loan entered into with Niagara Energy—as a result of the partial prepayment made on March 28, 2025, which entailed the settlement of interest accrued as of that date— and (ii) disbursements charged to the intercompany credit line totaling 11.5 million in Q2 and Q3 2025, which exceed the 1Q-4Q 10 million in principal corresponding to the local corporate bond repurchased in June 2025.

KEY OPERATIONAL DATA

- NET ENERGY GENERATION (GWh): It remained essentially stable compared to the first quarter of 2025 (+9 GWh; +0.5% Q1-Q3), due to higher thermal generation (95 GWh; +16.9 Q1-Q3), which offset lower hydroelectric production (-61 GWh; -5.9 Q1-Q3) and non-conventional renewable production (-25 GWh; -6.3 Q1-Q3). The latter were affected by less favorable hydrological conditions and lower levels of solar and wind resources.

- Energy sale (GWh): It decreased by 14.2% in Q3, primarily due to the expiration of contracts with regulated and non-regulated customers, against a backdrop of fewer contract renewals compared to previous years.